The 3-Account Setup, Step by Step

How to separate bills, spending and savings so one balance stops trying to explain your whole month.

Hi there,

Last week, I wrote about why a simple money system beats trying to remember everything.

The obvious next question is:

What does that system actually look like?

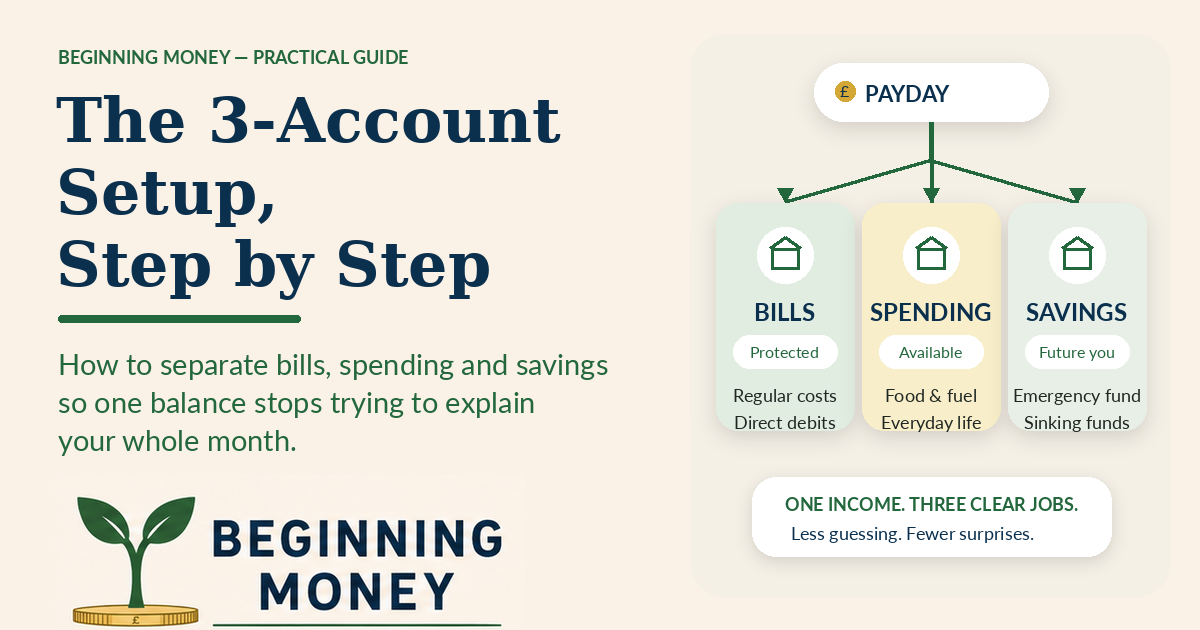

For me, the answer is three main accounts:

A bills account

A spending account

A savings account

That is not the only way to organise money.

It is not a revolutionary financial secret.

And nobody is going to hand you a small trophy for successfully opening three bank accounts.

But it gives each part of your money a clear job.

That matters because one bank balance can look simple while quietly trying to cover your entire life.

Mortgage or rent.

Council tax.

Food.

Fuel.

Debt payments.

Savings.

Birthdays.

Christmas.

School costs.

The occasional takeaway because nobody has the energy to cook.

One number cannot explain all of that clearly.

Three accounts can make it much easier.

Why separate the money?

The main benefit is not that three accounts create more money.

Unfortunately, banks have yet to add that feature.

The benefit is that separation reduces confusion.

When bills money sits in the same account as spending money, every purchase creates a small question:

Can I really afford this, or am I accidentally spending the electricity bill?

You may have £600 showing in the account.

But perhaps:

£180 is needed for bills

£150 is for food

£80 is for fuel

£100 is meant for savings

£60 is for an upcoming birthday

That leaves £30.

The balance says £600.

The reality says £30.

Separating the money helps those two numbers stop pretending to be the same thing.

Account 1: The Bills Account

The bills account is where the money for regular commitments lives.

This could include:

mortgage or rent

council tax

gas and electricity

water

broadband

mobile phones

insurance

childcare

subscriptions

debt minimum payments

any other regular direct debits

The basic rule is:

Once money enters the bills account, it is no longer available for everyday spending.

It already has a job.

That gives the account a clear purpose.

It also means the money sitting in your spending account is less likely to be mistaken for money needed elsewhere.

Work out the monthly bills figure

Start by listing every regular payment.

Use bank statements rather than memory.

Memory tends to remember the mortgage and forget the £7.99 subscription that has been quietly living its best life since 2022.

Include monthly bills and annual costs.

For annual bills, divide the total by 12.

For example:

Car insurance: £600 per year

Monthly amount: £50

You can either keep that £50 in the bills account or move it into a dedicated savings pot.

The important part is recognising that the bill exists before renewal day arrives.

Add a small buffer

If possible, leave a small amount extra in the bills account.

Not hundreds of pounds if that is unrealistic.

Even £20 or £30 can help absorb:

a slightly higher energy bill

a payment date moving

a forgotten direct debit

a small pricing increase

The buffer is not spending money.

It is there to stop the account operating with no margin at all.

Account 2: The Spending Account

The spending account is for normal day-to-day life.

This could include:

food

fuel

small household purchases

eating out

children’s activities

personal spending

day-to-day extras

This is the account you use regularly.

Its balance should represent money that is genuinely available to spend during the month.

That does not mean spending it all immediately.

It means you can use it without wondering whether the mortgage payment is hiding somewhere inside it.

Decide how often to fund it

You could transfer the full monthly amount on payday.

Or you could divide it into weekly amounts.

For example, if you have £800 available for monthly spending, you might transfer:

£800 once a month

£400 twice a month

£200 each week

Weekly transfers can be helpful if a full month’s spending money tends to disappear too quickly.

Monthly transfers are simpler if you are comfortable managing the full amount.

Neither method is morally superior.

Use the one that works with how you actually behave.

A technically perfect system that you abandon after nine days is not better than a basic system you keep using.

Keep the spending categories broad

You do not need a separate current account for food, fuel, coffees, toothpaste, socks and emergency biscuits.

That can turn a simple system into a full-time administrative role.

You might still use pots or track categories within the spending account, but the main job of this account is straightforward:

This is the money available for everyday life.

Account 3: The Savings Account

The savings account holds money that is not for immediate spending.

This might include:

an emergency fund

car maintenance

house repairs

birthdays

Christmas

holidays

annual subscriptions

clothes

school costs

other sinking funds

This is where savings pots can be useful.

The account itself holds the money.

The pots show what each part is for.

For example (savings pot and monthly amount):

Emergency fund: £100

Car maintenance: £50

Christmas: £40

Birthdays: £30

House maintenance: £50

Annual bills: £30

Emergency funds and sinking funds are different

They may sit in the same savings account, but they do different jobs.

An emergency fund is for something urgent and genuinely unexpected.

A sinking fund is for something expected but irregular.

A broken boiler may be an emergency.

Christmas is not.

It has turned up at roughly the same time every year for quite a while now.

Separating the two helps stop planned expenses repeatedly draining the emergency fund.

What happens on payday?

This is where the system becomes useful.

When income arrives, divide it before normal spending begins.

The order could look like this:

Step 1: Fund the bills account

Transfer enough to cover all regular commitments and any planned buffer.

Step 2: Fund the savings account

Move the agreed amounts into the emergency fund and sinking funds.

Step 3: Fund the spending account

Transfer what is available for normal day-to-day life.

The result is that the spending account shows a much more honest number.

Instead of asking:

How much money do we have?

You can ask:

How much do we have available for the rest of the month?

That is a much more useful question.

A simple worked example

Imagine £3,000 arrives on payday.

The monthly plan is (purpose and amount):

Bills account: £1,850

Savings account: £300

Spending account: £850

Total: £3,000

The £1,850 is protected for commitments.

The £300 is building future stability.

The £850 is available for day-to-day spending.

Nothing about the system changes the £3,000 income.

It simply makes each part visible.

That visibility can stop you spending money twice in your head.

What about joint finances?

The same structure can work for couples.

You might have:

one joint bills account

one joint spending account

one joint savings account

Or:

one joint bills account

personal spending accounts

shared savings pots

The best structure is the one both people understand.

If one person builds a complicated system and the other person needs a guided tour every time they buy petrol, the system is probably too complicated.

Both people should know:

what each account is for

how much goes into it

what can be spent

what should not be touched

when transfers happen

Clarity matters more than having the “perfect” arrangement.

Common mistakes to avoid

1. Moving too much into savings

Saving is good.

Moving so much into savings that you repeatedly move it back out again is less useful.

Set amounts you can genuinely maintain.

You can increase them later.

2. Forgetting irregular costs

Annual insurance, car servicing, birthdays and Christmas can make an otherwise sensible budget look broken.

They need to be included somewhere.

3. Creating too many pots

Pots can create clarity.

Too many can create another type of confusion.

Start with the biggest and most predictable costs.

Add more only when they solve a real problem.

4. Treating the bills account as spare money

A healthy-looking bills balance can be tempting.

But if the money is needed later in the month, it is not spare.

It is waiting.

5. Expecting the system to remove every difficult decision

A good system makes decisions clearer.

It does not make income unlimited.

There may still be months where the spending amount feels tight.

The difference is that you can see the problem instead of discovering it by accident.

How to set it up without overcomplicating it

You do not need to rebuild everything today.

Start with these steps:

List your regular bills.

Add up the monthly total.

Decide how much you want to set aside for future costs.

Work out what remains for everyday spending.

Give each amount a separate place.

Set up automatic transfers for payday.

Review it after one month.

The first version will not be perfect.

That is normal.

You may discover a bill you forgot.

You may set the food amount too low.

You may realise that one savings pot needs more and another needs less.

That is not failure.

It is the system becoming more accurate.

What I am learning

I used to think a bank balance was enough information.

It was not.

The number showed how much money was in the account.

It did not show:

what was already committed

what was being saved

what was needed later

what was genuinely available

Separating bills, spending and savings does not solve every financial problem.

But it gives the money clearer boundaries.

And clearer boundaries mean fewer surprises.

That is what I want from a money system.

Not perfection.

Not endless admin.

Just a clearer answer to the question:

What can this money safely be used for?

Your Turn

Look at the account where most of your money currently sits.

Could you separate it into three broad jobs?

bills

spending

savings

You do not need to open anything immediately.

Start by writing down how much belongs in each category.

That alone may show you more than the account balance does.

TL;DR

One bank balance can hide several different jobs.

A three-account setup separates money into:

Bills

Spending

Savings

The bills account protects regular commitments.

The spending account shows what is available for everyday life.

The savings account holds emergency money and planned future costs.

The system does not create more money.

It makes the money you have easier to understand.

What’s Next

Next week:

I’ll look at sinking funds: what they are, which ones are genuinely useful, and how to avoid creating so many pots that your banking app starts looking like a filing cabinet.

Until then,

Chris @ Beginning Money